Accountable: How big is the market?

Quantifying the Crypto Credit Market and Its Future Potential

➡ Why?

Credit isn't just another hype narrative that comes and goes. It's a fundamental pillar of how our world operates, and crypto is no exception. It drives market liquidity, supports innovation, and helps the entire ecosystem succeed. Without credit, growth and innovation are held back, limiting how much the market can develop.

If we look at traditional markets, the unsecured business loans market size was valued at $4.3 trillion in 2021 according to a report from Allied Market Research, and is projected to reach $12.5 trillion by 2031, growing at a CAGR of 11.7%.

Meanwhile, the crypto lending space peaked at less than 1.5% of the traditional market's volume in 2022. Although 2021 and 2022 highlighted the sector's potential, it has since taken a significant hit, contracting by 90% year-over-year in uncollateralized lending. Let’s be honest: the outlook is bleak, and there’s no immediate sign of recovery. Instead, many in the industry are now repackaging another settlement layer under a new label — whether it’s “we only lend to market makers” or “we only lend to fintech companies in Latin America.” However, these approaches often overlook critical questions: Who will be the lender? What can you offer them to invest in your opportunities? How will you restore trust?

We need fundamental changes in the credit ecosystem. Closing our eyes won’t make these challenges disappear.

👁️ How Did We Get Here?

Lenders, who are really just putting their capital to work, have become super cautious. A lot of this wariness comes from getting burned in the last market downturn and because borrowers aren't too keen — or sometimes even able — to fully open up about their trading moves or give up access to their wallets and APIs for monitoring. This lack of clear insight makes lenders nervous, and their response is pretty predictable: they tighten up the terms. They start asking for more collateral, bump up interest rates, and shrink the size of the loans they offer. While this strategy covers the lenders' backs, it puts borrowers in a tough spot.

On the flip side, borrowers find themselves struggling with higher costs and bigger collateral demands, which really ties their hands when it comes to effectively using loans. This hits market-neutral traders especially hard — they don’t play the usual buy and hold game and have to scrape together collateral from wherever they can, then cover their positions, which is anything but cheap or easy.

The end result? A vicious cycle where lenders are overly guarded, and borrowers are stuck under too much pressure. This imbalance points to a big problem in the digital asset market: we're not meeting the needs of lenders and borrowers effectively.

What’s clear is that both uncollateralized and undercollateralized lending need to make a comeback. If we’re betting on the future of crypto, we should also expect the crypto lending sector to grow. So why hasn’t it bounced back, even with rising prices? The answer lies in the shattered trust from the last cycle, driven by staggering levels of fraud, and the absence of a system to rebuild that trust between borrowers and lenders. This has to change. The market currently suffers from inefficiency due to the high levels of collateral required, which limits effective capital deployment.

Enhancing transparency is crucial, and recent technological advances now make it possible to address the privacy concerns that have long kept borrowers and lenders from finding common ground. Enabling trusted reporting without compromising sensitive information could be the key to unlocking un(der)collateralized lending and boosting the flow of capital in the credit markets, which benefits everyone involved. If Accountable doesn’t step up to this challenge, someone else will — because the ecosystem simply cannot expand without the support of robust credit solutions.

🔧 How Do We Solve It?

To navigate the delicate balance between transparency and privacy, the adoption of confidential computing techniques and zero-knowledge proofs presents a promising solution. Accountable enables the secure and private sharing of necessary information in a fully decentralized manner. It achieves this by running a mesh of self-sovereign nodes that process private data in a secure, encrypted environment, ensuring that sensitive information remains protected. Borrowers retain control of their API keys and data, sharing selected pieces of data live with lenders in a peer-to-peer fashion, complete with verifiability proofs attached.

By leveraging these techniques, it’s possible to increase the much-needed transparency in the lending process through the sharing of aggregated, non-specific data backed by verifiable computation and offer a comprehensive view of all assets and liabilities, both on-chain and off-chain. This ensures that while lenders receive enough information to make informed decisions, the borrowers’ most sensitive data, particularly their unique trading strategies, remain secure and undisclosed. This innovative approach can restore trust in the ecosystem, ensuring that lenders have the visibility they need without compromising the crucial intellectual property of borrowers. The end goal is to transform the ability to underwrite and monitor borrowers across diverse venues— from banks and crypto exchanges to custodians and wallets. This shift from relying on unaudited financial statements and screenshots to enabling live verification of borrowers' assets and trading exposures aims to significantly boost lenders' confidence.

On top of this solid foundation, which is trusted data, Accountable builds a Central Hub for Comprehensive Lending Solutions designed to facilitate borrower-lender interactions in a data-driven manner. This allows them to engage precisely as they desire, without being constrained to a specific label or market niche. A truly neutral infrastructure can unite lenders and borrowers from all segments of the market. Instead of creating another credit platform dedicated to one particular style of lending, we aim to provide our users with the tools they need to create the structures that work best for them. Our experience at M11 Credit taught us that a one-size-fits-all approach does not suit everyone; often, platform constraints made it extremely challenging to facilitate deals as desired. We need to let people innovate and make their lives easier instead of creating friction.

🧮 Where Are We Now?

We should start by analyzing the known market sizes of major players in the crypto lending space in 2022. This includes firms like Celsius, BlockFi, Genesis, and various DeFi lending platforms, which collectively represented approximately $30 billion in outstanding loans at their peak.

However, this figure captures only a portion of the total market. To derive a more comprehensive estimate, we considered additional significant segments, including:

Earning programs at exchanges: Major exchanges such as Coinbase and Kraken have their own lending desks, which contribute substantially to the total market volume.

Lending books of other major players: Companies like Nexo, Tether, and Galaxy Digital have substantial lending activities that are not always fully disclosed publicly.

Undisclosed institutional lending: Many transactions and loan agreements occur in less transparent settings, such as OTC, contributing further to the market size.

Given the partial visibility of these operations and the dynamic nature of the crypto market, we conservatively estimated that these additional segments at least double the visible market size, leading to an adjusted figure of approximately $60 billion. If we compare this to the traditional finance unsecured business loans market, which is about $4.3 trillion, crypto lending accounts for a bit less than 1.5%.

While this was the situation at the market’s peak, we are currently witnessing a significant decrease in activities, with no signs of recovery.

📈 Where Are We Going?

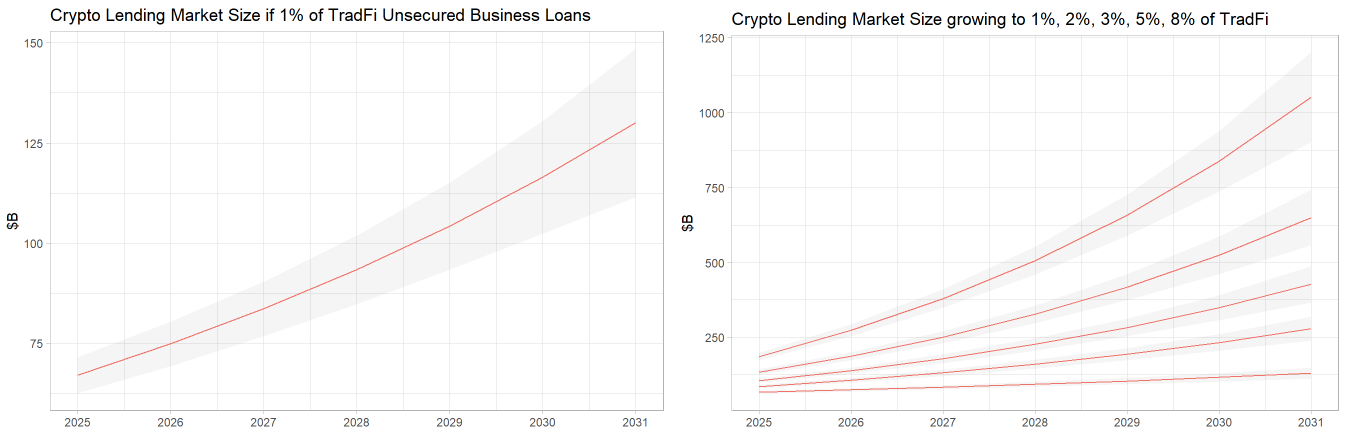

A strong case could be made that the crypto lending market's growth will surpass that of the traditional unsecured loans market, potentially witnessing a sharp recovery. However, let's start with the worst-case scenario: the crypto lending space grows at a similar 11.7% CAGR, as estimated by Allied Market Research for traditional finance, starting from what we assume is its lowest point of less than $10 billion. In this scenario, the crypto lending market would likely reach $25 billion by 2031. That would mean crypto credit represents less than 0.2% of the projected value for traditional finance. We believe this slow recovery is very unlikely. If crypto is to grow, the rise in the credit space will be much sharper. At the same time, to achieve this growth, restarting undercollateralized credit as a catalyst is imperative.

Let’s shift perspectives from a worst-case scenario to a more optimistic one, where we bet on crypto growing. What if crypto unsecured lending manages to rebuild trust in the system and captures 1% of the traditional unsecured business loans market by 2031? That would position us at around $130 billion.

Will the un(der)collateralized crypto lending market grow to be only 1% of the traditional market’s unsecured business loans? That’s less than it was in the previous cycle. What if it grows gradually and reaches 2%, 5%, or even 10% of it? We believe it is very likely for the market to expand at an accelerated pace and approach the 1 trillion mark by 2031. However, for that to happen, we need new, healthy foundations. Lenders will not return until we have a game-changing solution (hint: Accountable).

🔐 Could Accountable Be The Unlocking Factor?

We believe the answer is yes! Accountable's unique approach to data sharing empowers borrowers to control their data while simultaneously allowing lenders to see more. This includes revealing liabilities and restoring trust within our ecosystem, potentially unlocking idle capital.

Simply hoping that cash will return without any fundamental changes to business practices is futile. Lenders are unlikely to resume lending under the same conditions as before. However, increased transparency can catalyze a new era for crypto lending, and we are poised to lead this transformation. Currently, there is no other solution quite like ours in sight.

If Accountable becomes the game-changer it aims to be, it should be able to capture even just a fraction of this future market. While it's uncertain how large the market will grow and how much of it we can secure, our goal is to maximize our reach by becoming the industry standard for data sharing and the decentralized yet centralized hub for all credit-related activities. This will help glue back together the fragmented credit space and revitalize it.

Imagine if Accountable captures as little as 5% of the market by 2031 and charges 20 basis points for its services — it would already be a success. However, our ambitions stretch far beyond this. We aim to become the go-to place for credit business, drive innovation by enabling new credit structures, and facilitate the development of new protocols on top of our infrastructure.

Will Accountable be able to achieve this? We don't know for certain, but the prospects are promising. We believe in our vision and are committed to doing everything within our power to realize it.